3 things to do to boost your chances of getting an automatic credit limit increase

Using your credit card responsibly can have many positive impacts. One is that your credit line may automatically increase.

In just six months, my credit limit increased twice without any requests. That’s because I made on-time payments for over a year, always paid more than the minimum payment and had an income increase.

Even though a credit line increase cannot be guaranteed, here are some steps that you can take to increase your chances of qualifying for a higher limit.

What is a credit limit?

Your credit limit is the maximum amount of money that the creditor allows you to use on your new credit card. It is established based on your current credit quality.

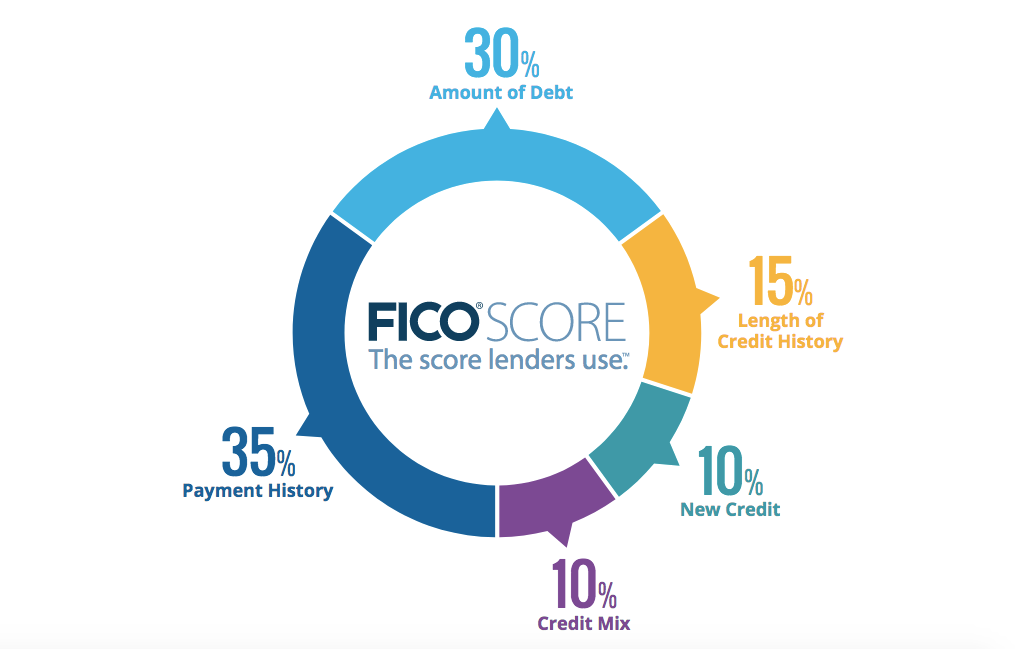

When card issuers set your credit limit, they take a look at a few factors, including:

After receiving an approval letter in the mail for a credit card, you will find a number indicating your credit limit. Alternatively, you can check your account online.

Anytime you make a purchase with your credit card, your available balance decreases. Conversely, when you make a payment on your credit card, your available balance increases. Over time, your credit limit will fluctuate based on your income and/or credit score.

What is a credit limit increase?

A credit limit increase means that you have more spending power than you previously had on your credit card. In turn, this will help increase your credit score.

How do I get an automatic credit limit increase?

Paying your credit card bill on time, keeping your credit card utilization low and maintaining a good credit score reveals that you can successfully manage your money. As a result, you may randomly see a credit limit increase when your issuer reviews your account.

Sign up for our daily newsletter

Each card issuer has different guidelines that will qualify you for an automatic credit limit increase when reviewing your account.

The goal is to make sure that you’re still practicing good credit habits. That means:

- Your credit card usage is under 30%: It is recommended that you pay your credit card in full at the end of each month. If you cannot do that, try to keep your credit utilization rate under 30%.

- You have no late payments: A rule of thumb to follow when using a credit card is to use it only if you have a repayment plan. If you don’t have a clear plan, try to refrain from making that purchase.

- You have sufficient income: If a credit card issuer does not see that your income will cover housing fees and debt, your credit limit won’t go up. Instead, it may decrease.

From time to time, creditors may increase your limit to reward you for on-time payments. They may not automatically boost your credit limit unless you have 6-12 months of on-time payments.

How does a higher credit limit help your credit score?

Your credit limit alone will not directly affect your score, but the amount you owe — your credit utilization — will have a large impact on your score.

A rule of thumb is to keep your credit utilization rate below 30%, but the lower the rate, the better. Anything higher than that number may serve as a red flag to creditors and can be a sign of financial distress.

If you have a balance on your card and your credit limit increases, your credit utilization will automatically drop. With credit card utilization counting for 30% of your overall score, an increased credit limit will increase your credit score.

Bottom line

Yes, it’s true — your credit limit can increase automatically without requesting it. Your chances of getting an automatic credit limit increase are boosted by keeping your credit utilization ratio low, paying your balances on time and having sufficient income.