Couple who want a simple retirement worry inflation will hurt plans

John is afraid inflation will eat away so much of his pension the couple will only have enough for groceries

Reviews and recommendations are unbiased and products are independently selected. Postmedia may earn an affiliate commission from purchases made through links on this page.

Article content

John* is ready to retire and not look back. The programming analyst has built his career with the federal government over the past 33 years and plans to retire at the end of this year.

Advertisement 2

Article content

“I’m 62 years old and I’m done with work, but I worry that inflation will eat away at my pension until it’s only enough for groceries.”

Article content

John currently earns about $90,000 a year before tax (about $60,000 after tax). His government defined-benefit pension plan is indexed to inflation and will pay $62,000 a year before tax if he retires as planned this year. Part of the pension is a bridged benefit to approximate Canada Pension Plan (CPP) payments until age 65.

Article content

His wife Cathy is 55 and works in the private sector. Her annual income is about $60,000 before tax. She plans to work another five to eight years before retiring. Her employer converted their once defined-benefit pension plan to a defined-contribution plan, so she used part of that money ($68,000) to purchase a car and put the rest in a locked-in retirement plan.

Advertisement 3

Article content

“It could take a while to pay back the pension money used to buy the car,” John said.

Each of them has about $60,000 in a registered retirement savings plan (RRSP) invested in moderate-risk mutual funds. They own a single-family home in Ottawa worth about $500,000, but don’t have a mortgage or any other big debts. John estimates their current monthly expenses run about $3,500 with the surplus income going into the bank and to “pay off” the pension money used to purchase the car.

My basic vision for retirement is that I stop working. I have very simple needs

John

The couple live modestly and have no big plans for retirement other than to pursue personal interests, as long as there’s enough money to do so.

“My basic vision for retirement is that I stop working. I have very simple needs,” John said. “I want to learn to play guitar. We don’t have any big travel plans in mind. It would be nice to be able to afford to travel, whether we do or not, is a different thing. Our last trip was to Disney World back in 2000.”

Article content

Advertisement 4

Article content

The couple don’t have children, but they would like to leave money to their nieces and nephews.

If they were to splurge, they’d like to purchase a swim spa, which would require some home renovations so it could be used year-round. John estimates it would cost between $80,000 and $100,000 and they would take out a mortgage on their house to do it. That said, their biggest priority is to ensure they’re comfortable in retirement.

“Is this going to work?” he asked.

What the experts say

Based on the numbers provided and their desired lifestyle, John and Cathy can both retire today, Ed Rempel, a fee-for-service financial planner, tax accountant and blogger, said.

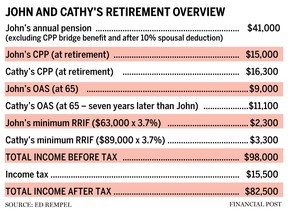

“Their current lifestyle expenses are about $3,500 a month, or $42,000 a year, which would require an income of $46,000 a year before tax,” he said. John’s pension alone is more than this.”

Advertisement 5

Article content

Eliott Einarson, a retirement planner at Ottawa-based Exponent Investment Management, agrees.

“I see this a lot in my own practice. People are looking for clarity on what’s possible,” he said. “They are debt free and John’s pension plus CPP and OAS (Old Age Security) when he claims them will likely come close to his current net income. They are fine.”

But Rempel is concerned they haven’t considered all their potential spending needs, such as entertainment, medical expenses, gifts, etc.

“I added an additional $2,500 a year for medical expenses assuming any health benefits stop when he retires, $5,000 for vacations and a $68,000 car every 10 years, assuming they want to keep a similar car to what they have and drive it for a long time,” he said. “This amounts to $56,000 a year — $64,000 before tax — or $4,700 a month to spend to achieve their desired retirement lifestyle.”

Advertisement 6

Article content

He recommends they take a closer look at the extra money (about $2,200) they have coming in each month. Right now, it’s not clear where it’s going. If they do nothing with it, they will slowly start to spend more and it will become part of their lifestyle spending.

Rempel recommends John split $18,000 of his pension with Cathy so they can both be in the lowest tax bracket. This will save $1,500 a year and ensure their OAS payments will not be clawed back.

“Both should convert their RRSPs to a registered retirement income fund and a life income fund, and start taking the minimum withdrawal when Cathy retires at 63 and John is 70,” he said.

As for when to claim CPP benefits, Rempel said the top two considerations are investment returns and tax.

Advertisement 7

Article content

“Since they invest in balanced mutual funds, their rate of return should be similar to CPP, about five per cent a year,” he said. “They will probably pay less tax if they start John’s CPP and OAS at age 70 when Cathy retires, and Cathy’s CPP at 63 when she retires and OAS at the earliest age of 65.”

Depending on its value, Einarson said it may make sense to not take the pension bridge John has access to and instead use his RRSP to overcome any gaps until he claims CPP, but the swim spa is well within their reach.

“Retirement is about cash flow. If expenses are only about $3,500, they could take out a line of credit or a mortgage and comfortably work that cost into their cash-flow needs,” he said. “It’s very doable, particularly if Cathy is going to continue working for the next seven to eight years. They could make sure the swim spa reno is paid off by the time she retires to feel an additional bit of safety.”

Advertisement 8

Article content

Einarson added that if they psychologically don’t mind having debt, they could take out a longer-term mortgage to pay off the spa upfront.

He also recommends investing their surplus income inside tax-free savings accounts.

-

Retired man living on cash savings making a mistake

-

Couple wants to retire early, hope government pensions enough

-

Can we retire on $170,000 and maintain our lifestyle?

“They are a great savings tool for the couple if they do need additional funds and also to build up money for the estate, which they could leave to their nieces and nephews,” he said.

*Names have been changed to protect privacy.

_____________________________________________________________

If you like this story, sign up for the FP Investor Newsletter.

_____________________________________________________________

Comments

Postmedia is committed to maintaining a lively but civil forum for discussion and encourage all readers to share their views on our articles. Comments may take up to an hour for moderation before appearing on the site. We ask you to keep your comments relevant and respectful. We have enabled email notifications—you will now receive an email if you receive a reply to your comment, there is an update to a comment thread you follow or if a user you follow comments. Visit our Community Guidelines for more information and details on how to adjust your email settings.

Join the Conversation